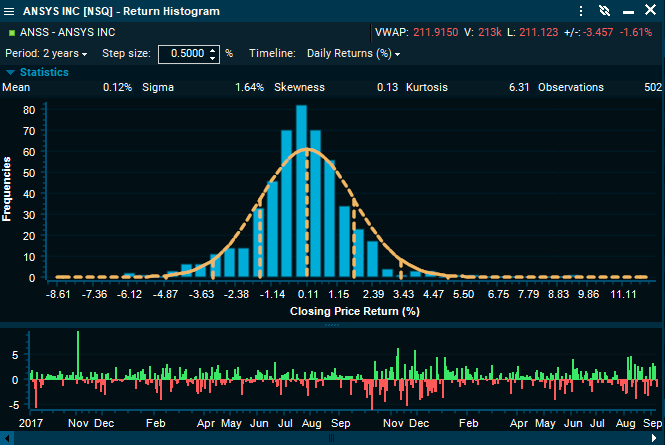

Return Histogram

How to access

Right-click an instrument > "Charts & Visualizations" > "Return Histogram".

How to use

This window displays the empirical distribution of the daily returns for a particular instrument or portfolio.

Period

Time series length. Options: "All", "LYTD" (last year to date), "YTD" (year to date), and 1 to 5 years. You can also specify a custom period by selecting "Custom".

Timeline

Allows the user to select the overview of the series in the lower panel. "Daily returns" displays the log returns in a bar chart, and "History" the actual values of the series.

Statistics bar

On the top of the histogram, the moments of the empirical distribution are displayed.

Element | Description |

|---|---|

Mean | Log daily returns. |

Sigma | Standard deviation from the log return series. |

Skewness | Standardized skewness of the empirical distribution as in Pearson's moment coefficient of skewness. |

Kurtosis | Excess kurtosis of the empirical distribution. |